Del 5

Del i serien Springer Finance

Financial Markets in Continuous Time

Häftad, Engelska, 2007

729 kr

Beställningsvara. Skickas inom 10-15 vardagar. Fri frakt för medlemmar vid köp för minst 249 kr.

Finns i fler format (1)

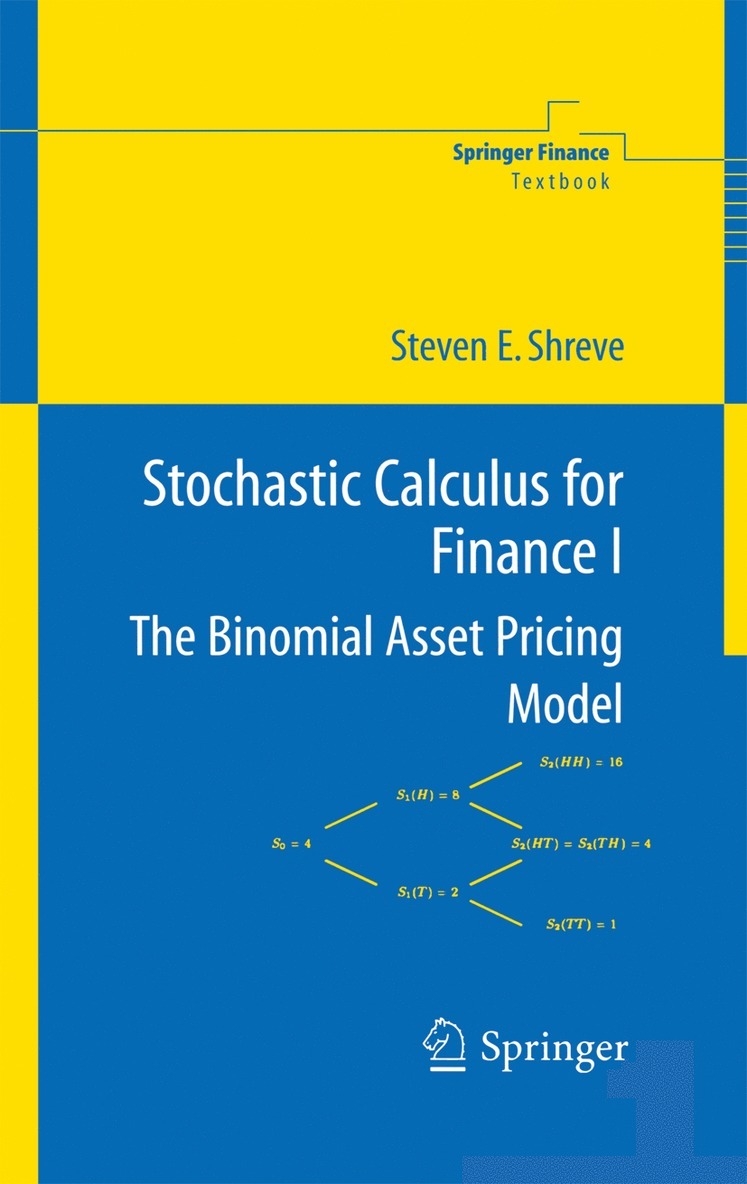

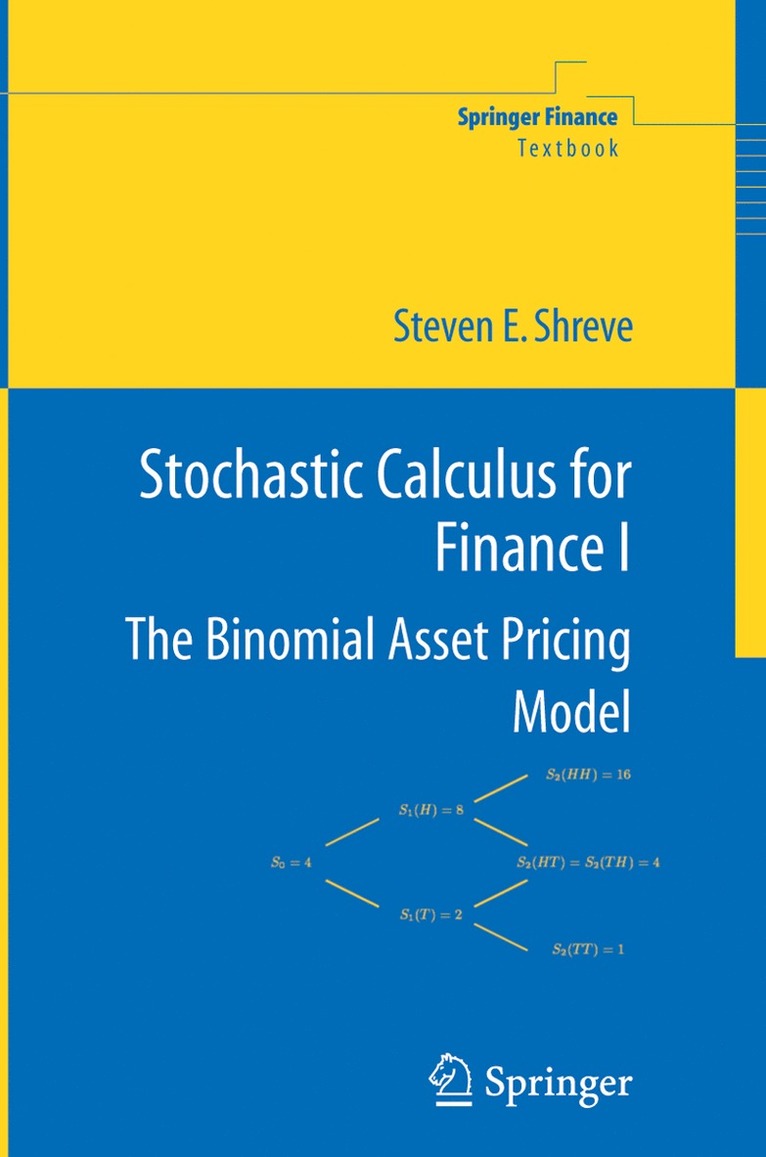

In modern financial practice, asset prices are modelled by means of stochastic processes, and continuous-time stochastic calculus thus plays a central role in financial modelling. This approach has its roots in the foundational work of the Nobel laureates Black, Scholes and Merton. Asset prices are further assumed to be rationalizable, that is, determined by equality of demand and supply on some market. This approach has its roots in the foundational work on General Equilibrium of the Nobel laureates Arrow and Debreu and in the work of McKenzie. This book has four parts. The first brings together a number of results from discrete-time models. The second develops stochastic continuous-time models for the valuation of financial assets (the Black-Scholes formula and its extensions), for optimal portfolio and consumption choice, and for obtaining the yield curve and pricing interest rate products. The third part recalls some concepts and results of general equilibrium theory, and applies this in financial markets. The last part is more advanced and tackles market incompleteness and the valuation of exotic options in a complete market.

Produktinformation

- Utgivningsdatum2007-07-12

- Mått155 x 235 x 19 mm

- Vikt517 g

- FormatHäftad

- SpråkEngelska

- SerieSpringer Finance

- Antal sidor324

- FörlagSpringer-Verlag Berlin and Heidelberg GmbH & Co. KG

- ISBN9783540711490

- ÖversättareA. Kennedy

Tillhör följande kategorier

Hoppa över listan

Mer från samma författare

Del 5

Dynamic Programming in Economics

Cuong Van, Rose-Anne Dana, Cuong Van, Rose-Anne Dana

Häftad, 2010

2 099 kr

Handbook on Optimal Growth 1

Rose-Anne Dana, Cuong Van, Tapan Mitra, Kazuo Nishimura

Inbunden, 2006

2 159 kr

Handbook on Optimal Growth 1

Rose-Anne Dana, Cuong Van, Tapan Mitra, Kazuo Nishimura

Häftad, 2010

2 099 kr

Hoppa över listan

Mer från samma serie

Derivative Securities and Difference Methods

You-lan Zhu, Xiaonan Wu, I-Liang Chern

Häftad, 2011

1 999 kr

Hoppa över listan

Du kanske också är intresserad av

Mathematical Methods for Financial Markets

Monique Jeanblanc, Marc Yor, Marc Chesney

Häftad, 2012

1 399 kr

Del 214

Actuarial Sciences and Quantitative Finance

Jaime A. Londoño, José Garrido, Monique Jeanblanc

Inbunden, 2017

1 399 kr

Del 5

Arbitrage, Credit And Informational Risks

Hillairet Caroline, Ying Jiao, Caroline Hillairet, Monique Jeanblanc

Inbunden, 2014

1 769 kr

Del 5

Handbook on Optimal Growth 1

Rose-Anne Dana, Cuong Van, Tapan Mitra, Kazuo Nishimura

Inbunden, 2006

2 159 kr

Handbook on Optimal Growth 1

Rose-Anne Dana, Cuong Van, Tapan Mitra, Kazuo Nishimura

Häftad, 2010

2 099 kr

Paris-Princeton Lectures on Mathematical Finance 2010

Areski Cousin, Stéphane Crépey, Olivier Guéant, David Hobson, Monique Jeanblanc, Jean-Michel Lasry, Jean-Paul Laurent, Pierre-Louis Lions, Peter Tankov, René Carmona, Erhan Çınlar, Ivar Ekeland, Elyès Jouini, Jose A. Scheinkman, Nizar Touzi

Häftad, 2010

709 kr

Del 5

Dynamic Programming in Economics

Cuong Van, Rose-Anne Dana, Cuong Van, Rose-Anne Dana

Häftad, 2010

2 099 kr